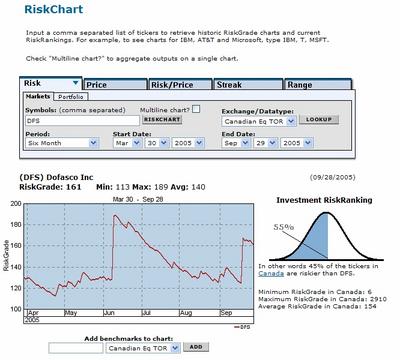

The last month has put Dofasco on the world stage, with bids coming in at a rapid rate, for an industry defined as "sunset" at best. Dofasco has some value, which of course is what TK and Arcelor see when they make the bids.

Of course, what they both see, and probably others, is QCM in Dofasco's pocket. Given the ore reserves and production, this will more than give a solid return on their bids, with the price of ore increasing for 2006.

However, Dofasco has been generous in their compensation plan with their employees...and keep in mind, anyone that puts out $5B for an investment, strategic or not, wants a return on their investment. Will Arcelor or TK get their return on the ore assets? I think so. But, you can't help but think that after Dofasco's $150 million charge against Q1 2005 for employees' compensation (refer to 2004 annual report), that after due diligence of the books, any suitor won't come in looking to make some changes to extract value for their shareholders.

It may be a year down the road, but I expect that changes may come for any suitor to maximize the return on their investment...with pressure from boards to provide 12-15% return, somehow Dofasco Inc. has to pony up $600-$750 million in gross earnings to contribute to the suitor's bottomline.

With the gap in steel prices and commodities closing, the only place left to squeeze value is in the operating costs.

23 December 2005

Arcelor Bids Again....$63 is the number

ARCELOR ENHANCES OFFER TO ACQUIRE DOFASCO INC.

23 December 2005 Companynews

(c) Copyright 2005 CompanynewsGroup. All rights reserved.

PRESS RELEASE Arcelor enhances offer to acquire Dofasco Inc. Luxembourg/Toronto - December 23rd, 2005 - Arcelor S.A. announces its intention to make an enhanced all cash offer to acquire all of the outstanding common shares of Canadian steelmaker Dofasco Inc. (TSX: DFS) at C$63.00 per share. Arcelor expects that the Board of Directors of Dofasco will recognize that this offer is superior to ThyssenKrupp's offer. Arcelor is open to approaches by Dofasco's Board of Directors and / or another party to finalize the acquisition at this attractive price level for the Dofasco Shareholders. Guy Dollé, Chief Executive Officer of Arcelor, reiterated that "Expansion into North America is a key strategic objective for Arcelor. We believe that Arcelor is an excellent partner for Dofasco. As a partner of the Arcelor group, Dofasco will become a stronger, more competitive steel producer on the North American steel market." Mr. Dollé also underlined that Dofasco's highly regarded corporate values with respect to its relations with employees, and its legacy of active community engagement, are principles that Arcelor shares and will continue to support. Full details of the offer will be included in the formal take-over bid and circular documents which Arcelor expects to mail to Dofasco shareholders in the coming days.

22 December 2005

2005 S&P Performance and 2006 Info

A good article wrapping up the year with the big winners and losers on the S&P 500 this year.

20 December 2005

Looking for a Bank Stock? Try Laurentian

Laurentian Bank has been on my watch list for a couple of months. It has gone up 12% in the last month. Estimated EPS of 2.33 (Oct 06), gives PE of 12.88...worth looking into.

19 December 2005

US Steel Value vs Dofasco

Came across this excerpt from Wall Street Journal Europe;

"Analysts say ThyssenKrupp's offer already is expensive, representing a 40% premium to Dofasco's share price before Arcelor launched its bid in November. In a recent report, Morgan Stanley estimated ThyssenKrupp's offer values Dofasco's steel capacity at about $1,000 a ton, while U.S. Steel Corp. trades at about $350 a ton."

As I had blogged earlier in the month, US Steel won't command the same price as Dofasco. With the difference in value, and other factors, I would like to see USX improve their results. So does Citigroup. Other agencies are soon to follow.

"Analysts say ThyssenKrupp's offer already is expensive, representing a 40% premium to Dofasco's share price before Arcelor launched its bid in November. In a recent report, Morgan Stanley estimated ThyssenKrupp's offer values Dofasco's steel capacity at about $1,000 a ton, while U.S. Steel Corp. trades at about $350 a ton."

As I had blogged earlier in the month, US Steel won't command the same price as Dofasco. With the difference in value, and other factors, I would like to see USX improve their results. So does Citigroup. Other agencies are soon to follow.

Comment Question - Nortel Stock or Options?

Thanks for the comment, Anonymous. I was thinking about how best to give you my opinion on what I would do.

Here is a good article that gives the general concepts for others considering options trading;

http://www.investopedia.com/articles/optioninvestor/03/073003.asp

Because of the volatility with the company right now, I have no doubt that the stock price would rise over the next 6 months for a substantial gain (beats indices). However, with all the management changes going on right now with Nortel, and other factors (growth, etc.), I think that the options for Nortel are risky right now...what I think is, there are more variables affecting the volatility than what can be accurately predicted.

That being said, sure, if you had some money you wanted to risk, and after understanding all the volatility behind the premium, then yes, I would do it. The one thing that would hold me up personally right now, is that I don't have a portfolio diverse enough to take the risk. Its also hard to answer your question without understanding more of the contracts you are considering.

To put in perspective, I would option HP before Nortel, based on the what I see. With increased volatility, comes increased risk and reward.

Here is a blog I read every day, Phil's World, which gives you a good handle on what all is involved with options trading. Read about his risks and rewards.

Here is a good article that gives the general concepts for others considering options trading;

http://www.investopedia.com/articles/optioninvestor/03/073003.asp

Because of the volatility with the company right now, I have no doubt that the stock price would rise over the next 6 months for a substantial gain (beats indices). However, with all the management changes going on right now with Nortel, and other factors (growth, etc.), I think that the options for Nortel are risky right now...what I think is, there are more variables affecting the volatility than what can be accurately predicted.

That being said, sure, if you had some money you wanted to risk, and after understanding all the volatility behind the premium, then yes, I would do it. The one thing that would hold me up personally right now, is that I don't have a portfolio diverse enough to take the risk. Its also hard to answer your question without understanding more of the contracts you are considering.

To put in perspective, I would option HP before Nortel, based on the what I see. With increased volatility, comes increased risk and reward.

Here is a blog I read every day, Phil's World, which gives you a good handle on what all is involved with options trading. Read about his risks and rewards.

18 December 2005

Update - Miscellaneous

A few notes on what I am watching;

- RIM is still having its legal problems. Earlier this month, I figured a target of $62 for RIM. With the courts ruling against RIM, I still maintain it will go lower ($1 billion settlement to NTP, and expensive licensing arrangement). Stay tuned.

- Stelco, well, what can be said about it. Shareholder value has been all but wiped out. With the new shares under the restructuring plan having a value of $5.50, steel prices softening in Q1, I don't expect big things from them.

- Dofasco hit the $64 mark...might be a good idea to take it now. Even though Arcelor is going to act or react sometime this year, going into the holidays and into the new year, I don't think there will be any surprises.

- Sony is still on my watch list - I can't help but think that it will be a bargain some time in the first 6 months of 2006.

- Nortel is being sluggish. No surprise there with the changes in management.

- Vincor, having defeated the Constellation takeover, still feels that Constellation's bid was oppurtunistic - I agree. Again, we'll see what happens with next quarter results.

- Laurentian Bank has been on my watch list for the last 3 months - steady gains over the last 4 weeks make it a good buy.

Personal Thoughts - GM

No surprise these days with the doom and gloom over GM. Interesting to note - stock is at a decades low, and without the suspension of the dividend, it has a nice return (about 9%). Some analysts are suggesting a "buy" on GMAC bonds that gives a little bit higher return. Is GM stock worth a risk? I think so.

Seems that GM is going in spurts these last 4 quarters. My thoughts are that the new models might actually spurn some spending in the new year, within the first 6 months anyways. With Kerkorian getting his seat on the board, and a mediocre restructuring plan, I think its possible to get some value out of the stock for the next 6 months.

The big thing missing in GM's plan, is exciting models. Keep in mind GM, that stylish, affordable, reliable cars are what the public needs. GM is not in a position to challenge DCX with designs like the 300. The formula has worked well for Toyota and Honda, both which started out with the affordable/reliable route first, before they moved into styling and going after market segments.

GM, remember the KISS method - Keep it Simple, Stupid. I'll revisit GM down the road, pending developments with Delphi too.

Seems that GM is going in spurts these last 4 quarters. My thoughts are that the new models might actually spurn some spending in the new year, within the first 6 months anyways. With Kerkorian getting his seat on the board, and a mediocre restructuring plan, I think its possible to get some value out of the stock for the next 6 months.

The big thing missing in GM's plan, is exciting models. Keep in mind GM, that stylish, affordable, reliable cars are what the public needs. GM is not in a position to challenge DCX with designs like the 300. The formula has worked well for Toyota and Honda, both which started out with the affordable/reliable route first, before they moved into styling and going after market segments.

GM, remember the KISS method - Keep it Simple, Stupid. I'll revisit GM down the road, pending developments with Delphi too.

Well-Rested and Ready to Go

Sorry for the lack of entries this week, but I was away on a much needed vacation. Thank you to all of you that come back on a regular basis. I will be doing more entries over the holidays, while I am off work. There are always interesting things happening in financial markets that are worth comments.

Stay tuned!

Stay tuned!

11 December 2005

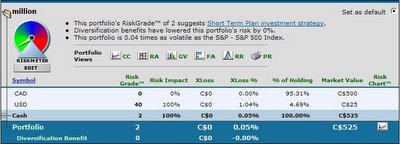

Updated Portfolio - 9 Dec 05

Just an update of my portfolio, which of course, is still all cash until the new year;

$624...another $999,376 to go.

$624...another $999,376 to go.

$624...another $999,376 to go.

$624...another $999,376 to go.

10 December 2005

Inside Scoop on What Happened with Dofasco

I came across this article, which basically gives all the details as to what happened with Dofasco...

Dofasco board shows steel in Thyssen deal: Behind the scenes, board and advisors forced higher offer

Sandra Rubin

Financial Post 7 December 2005

National Post National FP9(c) 2005 National Post . All Rights Reserved.

We were interested to see reports last week that Dofasco CEO Don Pether took it on the chin from some hedge funds for signing a $61.50 a share friendly deal with ThyssenKrupp instead of soliciting higher bids. Mr. Pether's tongue must have been bleeding. What they didn't know, and he couldn't say, is that Dofasco's management and financial advisers had personally contacted all the usual steel industry suspects to ask them if they wanted to mount a bid -- and got Thyssen to up its own bid at least twice and cut the break fee in half before signing a deal.

The whole saga started May 27 with a $43 a share joint offer from the Luxembourg-based steelmaker Arcelor and U.S. steelmaker Nucor Corp.

People thought the sale was going to go ahead then. In fact, we hear Jon Levin, who was working with Joan Weppler, Dofasco's vice-president and general counsel, and a Fasken Martineau team that included Wally Palmer and Sean Stevens, actually cancelled his summer vacation. (For those of you who don't have your list handy, that's No. 17 on the Top 50 Ways to Make Yourself Popular at Home. It's a Category 33.6 offence, punishable by jewelry.)

When the $43 offer landed, Dofasco retained a team led by Peter Buzzi at RBC Dominion Securities to provide a fairness opinion and its view can be distilled thus: unfair. A short time later, the Arcelor group, which was being advised by a team at Ogilvy Renault headed by Marc Lacourciere and Terry Dobbin, upped its bid to $46 in cash plus a share of Quebec Cartier Mines.

Things really only heated up Nov. 10 when Arcelor and Nucor (being advised on the financial side by Jim Kofman and David Bain of UBS Securities) sent Dofasco a letter saying they were willing to pay $52 a share if the bid was hostile, and $55 for a friendly bid that allowed them to do due diligence.

Oh, and at that point Arcelor threatened to circumvent the board and go directly to shareholders. The board thought about it over the weekend and met Monday, Nov. 14 to discuss the situation. They sent the Arcelor group a return letter, saying the latest offer didn't appear to fully value the company. They suggested the group meet with Dofasco's financial advisers.

Nov. 16, Dofasco's special committee met and asked Mr. Pether to contact ThyssenKrupp to see if the German company would be interested in making an offer.

The two companies had been looking at doing some joint ventures together -- and Mr. Pether had had a rather interesting conversation a few months earlier with Ekkehard Schulz, ThyssenKrupp's executive chairman. It went something like this.

Dr. Schultz: "You know, Don, I've been thinking. We've been looking at doing business for some time. I like you. I like your company. And I think we'd want to make a bid for Dofasco if someone put you in play by making a hostile run at you -- assuming, of course, you think that's appropriate."

Mr. Pether: "Ekkehard, if we're on the wrong end of a hostile, there's no one I'd rather have as my white knight." Maybe Dr. Schulz consulted Madame Imakamyownlucka, the noted public-company psychic. Maybe it was just fortuitous. All we can tell you is such a conversation actually took place.

In the meantime, Arcelor and Nucor advised Dofasco it could chose from either the group's two previous bids -- one of which was as high as $55.

Mr. Pether telephoned Dr. Schulz to inform him of the hostile bid. Dr. Schulz said he'd call Dofasco back the next day. It's safe to assume he called Mark Trachuk of Osler Hoskin & Harcourt right after hanging up. Mr. Trachuk and Oslers had been working with Thyssen since last summer on making a potential Canadian acquisition.

Mr. Trachuk called in Lorraine Lynds among others at Oslers, while Jonathan White of Citigroup in London and Mary Amor at Citigroup in New York were mobilized to provide financial advice.

The next day, Nov. 17, Dr. Schulz advised Mr. Pether that ThyssenKrupp was interested in making a proposal, and a management team would fly to Toronto for a meeting with Dofasco and its advisers the following day.

Dofasco's special committee informed the full board of ThyssenKrupp's interest, and advised the board that based on the advice of their financial advisers, they were rejecting the revised Arcelor bid.

Dr. Schulz and his team arrived as promised Nov. 18. There were meetings. They went well. Dofasco and Thyssen signed a confidentiality and standstill agreement and Thyssen was given access to non-public financial information.

The board told Arcelor that its bid had been rejected. Later that day, DS advised the board on what it felt would be an appropriate price. Someone, somewhere, among the advisers was also providing advice on what would be an appropriate menu.

The two management teams had a clandestine dinner in one of Oslers' board rooms. No lawyers, no bankers -- and no restaurant. "It had to remain secret," says someone who knows. "They really hit it off. The social dynamics are important in these types of things."

Nov. 21, Dr. Schulz wrote Mr. Pether formally indicating Thyssen was prepared to outbid Arcelor, with a deal that included a $200-million break-fee. Dofasco looked at the offer and told Thyssen it wasn't high enough. At that point, Arcelor was still at the table offering to bid more. The next day, it did.

Nov. 22 Arcelor and Nucor submitted what they said was their "final offer," a complex cash and share deal. What they didn't know is Dofasco already had a higher bid.

ThyssenKrupp, meanwhile, upped its price. Dofasco's board met, reviewed the bids, and decided Thyssen's was clearly better although it felt the break-fee was too high and the price was still too low.

In the wee hours of Nov. 23, we're talking 1 a.m., Arcelor issued a press release going public with an all-cash bid of $56, which was higher than previously indicated. Later that morning, Dofasco got a letter from ThyssenKrupp topping its previous offer, and Arcelor's publicized offer as well.

Dofasco again sent it back, saying it was still too low. Dofasco's board met later that morning and decided the Thyssen offer was approaching the magic number, but directors were concerned the break-fee was too high. The board held a discussion on the risks and benefits of conducting a full auction.

We imagine Dofasco's advisers would have told them that with the company in play, they would be smart to contact other strategic buyers to make sure there were no other interested parties.

The board meeting adjourned. Phone calls were made. The responses were lukewarm at best. When the board met again that afternoon, it was told that Dofasco management and its financial advisers had contacted a number of steel companies and none indicated an immediate or strong desire to enter into significant discussions to buy the company.

Later that day, Thyssen came back at $61.50 plus a lowered $100-million break-fee. The deal looked pretty attractive. Dofasco's board decided to give Thyssen an exclusivity agreement good until Dec. 5 to do due diligence.

Thyssen went in, had a look, and informed Dofasco on Saturday, Nov. 26 that it didn't need until Dec. 5. The company asked Dofasco if it would be ready to sign and announce on the morning of Monday, Nov. 28.

Everyone, of course, had coteries of tax lawyers, competition-law lawyers, and Investment Canada types involved. But the bottom line is the $5-billion deal was drafted, documented and negotiated in five days. And some people wonder why some people have God complexes. . . .

Dofasco board shows steel in Thyssen deal: Behind the scenes, board and advisors forced higher offer

Sandra Rubin

Financial Post 7 December 2005

National Post National FP9(c) 2005 National Post . All Rights Reserved.

We were interested to see reports last week that Dofasco CEO Don Pether took it on the chin from some hedge funds for signing a $61.50 a share friendly deal with ThyssenKrupp instead of soliciting higher bids. Mr. Pether's tongue must have been bleeding. What they didn't know, and he couldn't say, is that Dofasco's management and financial advisers had personally contacted all the usual steel industry suspects to ask them if they wanted to mount a bid -- and got Thyssen to up its own bid at least twice and cut the break fee in half before signing a deal.

The whole saga started May 27 with a $43 a share joint offer from the Luxembourg-based steelmaker Arcelor and U.S. steelmaker Nucor Corp.

People thought the sale was going to go ahead then. In fact, we hear Jon Levin, who was working with Joan Weppler, Dofasco's vice-president and general counsel, and a Fasken Martineau team that included Wally Palmer and Sean Stevens, actually cancelled his summer vacation. (For those of you who don't have your list handy, that's No. 17 on the Top 50 Ways to Make Yourself Popular at Home. It's a Category 33.6 offence, punishable by jewelry.)

When the $43 offer landed, Dofasco retained a team led by Peter Buzzi at RBC Dominion Securities to provide a fairness opinion and its view can be distilled thus: unfair. A short time later, the Arcelor group, which was being advised by a team at Ogilvy Renault headed by Marc Lacourciere and Terry Dobbin, upped its bid to $46 in cash plus a share of Quebec Cartier Mines.

Things really only heated up Nov. 10 when Arcelor and Nucor (being advised on the financial side by Jim Kofman and David Bain of UBS Securities) sent Dofasco a letter saying they were willing to pay $52 a share if the bid was hostile, and $55 for a friendly bid that allowed them to do due diligence.

Oh, and at that point Arcelor threatened to circumvent the board and go directly to shareholders. The board thought about it over the weekend and met Monday, Nov. 14 to discuss the situation. They sent the Arcelor group a return letter, saying the latest offer didn't appear to fully value the company. They suggested the group meet with Dofasco's financial advisers.

Nov. 16, Dofasco's special committee met and asked Mr. Pether to contact ThyssenKrupp to see if the German company would be interested in making an offer.

The two companies had been looking at doing some joint ventures together -- and Mr. Pether had had a rather interesting conversation a few months earlier with Ekkehard Schulz, ThyssenKrupp's executive chairman. It went something like this.

Dr. Schultz: "You know, Don, I've been thinking. We've been looking at doing business for some time. I like you. I like your company. And I think we'd want to make a bid for Dofasco if someone put you in play by making a hostile run at you -- assuming, of course, you think that's appropriate."

Mr. Pether: "Ekkehard, if we're on the wrong end of a hostile, there's no one I'd rather have as my white knight." Maybe Dr. Schulz consulted Madame Imakamyownlucka, the noted public-company psychic. Maybe it was just fortuitous. All we can tell you is such a conversation actually took place.

In the meantime, Arcelor and Nucor advised Dofasco it could chose from either the group's two previous bids -- one of which was as high as $55.

Mr. Pether telephoned Dr. Schulz to inform him of the hostile bid. Dr. Schulz said he'd call Dofasco back the next day. It's safe to assume he called Mark Trachuk of Osler Hoskin & Harcourt right after hanging up. Mr. Trachuk and Oslers had been working with Thyssen since last summer on making a potential Canadian acquisition.

Mr. Trachuk called in Lorraine Lynds among others at Oslers, while Jonathan White of Citigroup in London and Mary Amor at Citigroup in New York were mobilized to provide financial advice.

The next day, Nov. 17, Dr. Schulz advised Mr. Pether that ThyssenKrupp was interested in making a proposal, and a management team would fly to Toronto for a meeting with Dofasco and its advisers the following day.

Dofasco's special committee informed the full board of ThyssenKrupp's interest, and advised the board that based on the advice of their financial advisers, they were rejecting the revised Arcelor bid.

Dr. Schulz and his team arrived as promised Nov. 18. There were meetings. They went well. Dofasco and Thyssen signed a confidentiality and standstill agreement and Thyssen was given access to non-public financial information.

The board told Arcelor that its bid had been rejected. Later that day, DS advised the board on what it felt would be an appropriate price. Someone, somewhere, among the advisers was also providing advice on what would be an appropriate menu.

The two management teams had a clandestine dinner in one of Oslers' board rooms. No lawyers, no bankers -- and no restaurant. "It had to remain secret," says someone who knows. "They really hit it off. The social dynamics are important in these types of things."

Nov. 21, Dr. Schulz wrote Mr. Pether formally indicating Thyssen was prepared to outbid Arcelor, with a deal that included a $200-million break-fee. Dofasco looked at the offer and told Thyssen it wasn't high enough. At that point, Arcelor was still at the table offering to bid more. The next day, it did.

Nov. 22 Arcelor and Nucor submitted what they said was their "final offer," a complex cash and share deal. What they didn't know is Dofasco already had a higher bid.

ThyssenKrupp, meanwhile, upped its price. Dofasco's board met, reviewed the bids, and decided Thyssen's was clearly better although it felt the break-fee was too high and the price was still too low.

In the wee hours of Nov. 23, we're talking 1 a.m., Arcelor issued a press release going public with an all-cash bid of $56, which was higher than previously indicated. Later that morning, Dofasco got a letter from ThyssenKrupp topping its previous offer, and Arcelor's publicized offer as well.

Dofasco again sent it back, saying it was still too low. Dofasco's board met later that morning and decided the Thyssen offer was approaching the magic number, but directors were concerned the break-fee was too high. The board held a discussion on the risks and benefits of conducting a full auction.

We imagine Dofasco's advisers would have told them that with the company in play, they would be smart to contact other strategic buyers to make sure there were no other interested parties.

The board meeting adjourned. Phone calls were made. The responses were lukewarm at best. When the board met again that afternoon, it was told that Dofasco management and its financial advisers had contacted a number of steel companies and none indicated an immediate or strong desire to enter into significant discussions to buy the company.

Later that day, Thyssen came back at $61.50 plus a lowered $100-million break-fee. The deal looked pretty attractive. Dofasco's board decided to give Thyssen an exclusivity agreement good until Dec. 5 to do due diligence.

Thyssen went in, had a look, and informed Dofasco on Saturday, Nov. 26 that it didn't need until Dec. 5. The company asked Dofasco if it would be ready to sign and announce on the morning of Monday, Nov. 28.

Everyone, of course, had coteries of tax lawyers, competition-law lawyers, and Investment Canada types involved. But the bottom line is the $5-billion deal was drafted, documented and negotiated in five days. And some people wonder why some people have God complexes. . . .

Latest on Stelco

Last night, all the creditors approved the restructuring plan. So, it seems that the battle for shares is heating up, which was the big roadblock for creditors to accept the plan. There is speculation that the creditors are jockeying for position to hold more shares now, due to the interest in Dofasco and the premium offered by TK...will Stelco get the same deal? I don't think the world players are going to make a bid for Stelco any time soon...no concessions from the unions through this process still makes it unattractive at this time. Stelco is going to need some cash to pay its bills next year, to the pension fund. With a slight steel glut coming in the second quarter 2006, it will be difficult for Stelco to meet its obligations. See how things go, I wish them luck.

09 December 2005

Vincor - All Hope is Not Lost

Reviewing the latest news, Vincor has dropped on the expiration of Constellation's last offer of $35...below is a quote pulled from Reuters;

Vincor, which has brands such as Inniskillin and Jackson-Triggs, has said a bid between C$39.33 and C$76.14 a share was adequate to gain access to its confidential data.

So, $40 might be a reasonable comeback bid from Constellation in the new year...as I said before, see how the next quarterly results pan out for Vincor.

Vincor, which has brands such as Inniskillin and Jackson-Triggs, has said a bid between C$39.33 and C$76.14 a share was adequate to gain access to its confidential data.

So, $40 might be a reasonable comeback bid from Constellation in the new year...as I said before, see how the next quarterly results pan out for Vincor.

Current News on Stelco Plan

Interesting article on the status of the current Stelco plan on the table for a vote today...courtesy of the Hamilton Spectator

Stelco offering voters new deal

Steve Arnold

The Hamilton Spectator9 December 2005

The Hamilton Spectator Final

A01Copyright (c) 2005 The Hamilton Spectator.

Intense negotiations have produced a new restructuring plan for Stelco. The latest proposal, the fourth plan this month aimed at ending nearly two years of bankruptcy protection, was approved yesterday by the board of directors. It goes to a vote of creditors today.

Previous plans had tried to satisfy two very different demands from bondholders. First, they wanted cash in addition to new debentures. Then, when a German steelmaker offered $4.8 billion for Dofasco, they demanded new shares that they could sell to any buyer in the market for Stelco.

This plan tries to satisfy both. Under it, Stelco creditors will get a pro-rated share of $275 million in new notes, more than $106 million in cash, 1.1million common shares and the right to draw from a pool of more than 5.6 million new shares which can either be held or sold to equity investors for $5.50 each.

In an interview, Stelco president Courtney Pratt said he's hopeful this version will be the one that finally ends the company's long nightmare by letting creditors choose how they will be paid.

"The changes are very specifically responding to bondholder concerns and give them the opportunity to take shares rather than cash," he said. "They have the option with this plan."

While Stelco's bondholders helped negotiate the newest plan, Pratt said none had committed to supporting it. "Right now, I don't know what the vote will be, but I am hopeful that we'll get a yes vote because we've listened and we've restructured the plan," he said. "I hope these changes will be what's required to get us a yes vote but it's still possible that this plan could be further amended before we take the vote."

Under Stelco's bankruptcy protection, creditors holding two-thirds of its $640-million debt must vote in favour of a restructuring plan which will then be taken to Superior Court Justice James Farley for final approval. Failure to get creditor support could result in a court-ordered sale of the company or a push into receivership by operating creditors if the protection order is not extended at the company's next court appearance on Monday.

Court documents for the sale have been prepared by the United Steel Workers and the motion for a receiver has been filed by Stelco's operating lenders, owed about $217 million.

The pool of new shares to be offered creditors was created by Tricap Management Limited and two investment partners agreeing to give up some of the stake in Stelco they were to get in exchange for lending the company $375 million. Those investors have agreed to buy almost 19.4 million new Stelco shares for more than $106.5 million to prime the pool from which creditors will draw. Any shares left in the pool by creditors will then be purchased by the investors, potentially topping the fund up to $137.5 million.

Elements unchanged from previous plans include paying $400 million toward Stelco's $1.3-billion pension deficit and providing money for new equipment the company says is vital to reducing its production costs. Much of the pension downpayment will come as a forgivable loan of $150 million from the provincial government. Ottawa is also kicking in $30 million for energy projects.

The balance of the pension shortfall will be settled over 10 years with annual payments of $65 million for five years and $70 million for five years starting in the second half of 2006.

Existing shareholders get nothing. Voting on the new plan will be conducted at the International Centre in Mississauga, starting at 10 a.m. In a letter to employees yesterday, Pratt said failure to reach a deal doesn't mean plant gates will be locked immediately and "your wages, benefits and other terms of employment will continue in their current form.

Stelco's directors Wednesday rejected a plan put forward by bondholders. That would have seen Tricap allowed to buy 10 million new shares for $5.50 each. That money would go to creditors along with 15 million shares which senior debenture holders could then buy for $5.50 each. Creditors would also share in $275 million of secured notes and an additional 1.1 million common shares.

If Tricap dropped out of Stelco's refinancing, the bondholders offered to arrange their own package. In another development yesterday, Stelwire workers in Hamilton voted 95 per cent in favour of a deal with the plant's new owner. Stelwire, with plants in Hamilton and Burlington, is one of the subsidiaries being sold by Stelco.

The pact will see the company's Burlington operation close and work consolidated in Hamilton. It includes an early retirement incentive that will allow workers age 55 with 15 years service to leave with a full pension.

"People are happy with this because we're going to restructure and put the business back on its feet," said union president Scott Duvall. "We're sad to be leaving the Stelco chain after 50 years, but we know we have to move on. Settling this will be a real burden off people's minds."

Stelco offering voters new deal

Steve Arnold

The Hamilton Spectator9 December 2005

The Hamilton Spectator Final

A01Copyright (c) 2005 The Hamilton Spectator.

Intense negotiations have produced a new restructuring plan for Stelco. The latest proposal, the fourth plan this month aimed at ending nearly two years of bankruptcy protection, was approved yesterday by the board of directors. It goes to a vote of creditors today.

Previous plans had tried to satisfy two very different demands from bondholders. First, they wanted cash in addition to new debentures. Then, when a German steelmaker offered $4.8 billion for Dofasco, they demanded new shares that they could sell to any buyer in the market for Stelco.

This plan tries to satisfy both. Under it, Stelco creditors will get a pro-rated share of $275 million in new notes, more than $106 million in cash, 1.1million common shares and the right to draw from a pool of more than 5.6 million new shares which can either be held or sold to equity investors for $5.50 each.

In an interview, Stelco president Courtney Pratt said he's hopeful this version will be the one that finally ends the company's long nightmare by letting creditors choose how they will be paid.

"The changes are very specifically responding to bondholder concerns and give them the opportunity to take shares rather than cash," he said. "They have the option with this plan."

While Stelco's bondholders helped negotiate the newest plan, Pratt said none had committed to supporting it. "Right now, I don't know what the vote will be, but I am hopeful that we'll get a yes vote because we've listened and we've restructured the plan," he said. "I hope these changes will be what's required to get us a yes vote but it's still possible that this plan could be further amended before we take the vote."

Under Stelco's bankruptcy protection, creditors holding two-thirds of its $640-million debt must vote in favour of a restructuring plan which will then be taken to Superior Court Justice James Farley for final approval. Failure to get creditor support could result in a court-ordered sale of the company or a push into receivership by operating creditors if the protection order is not extended at the company's next court appearance on Monday.

Court documents for the sale have been prepared by the United Steel Workers and the motion for a receiver has been filed by Stelco's operating lenders, owed about $217 million.

The pool of new shares to be offered creditors was created by Tricap Management Limited and two investment partners agreeing to give up some of the stake in Stelco they were to get in exchange for lending the company $375 million. Those investors have agreed to buy almost 19.4 million new Stelco shares for more than $106.5 million to prime the pool from which creditors will draw. Any shares left in the pool by creditors will then be purchased by the investors, potentially topping the fund up to $137.5 million.

Elements unchanged from previous plans include paying $400 million toward Stelco's $1.3-billion pension deficit and providing money for new equipment the company says is vital to reducing its production costs. Much of the pension downpayment will come as a forgivable loan of $150 million from the provincial government. Ottawa is also kicking in $30 million for energy projects.

The balance of the pension shortfall will be settled over 10 years with annual payments of $65 million for five years and $70 million for five years starting in the second half of 2006.

Existing shareholders get nothing. Voting on the new plan will be conducted at the International Centre in Mississauga, starting at 10 a.m. In a letter to employees yesterday, Pratt said failure to reach a deal doesn't mean plant gates will be locked immediately and "your wages, benefits and other terms of employment will continue in their current form.

Stelco's directors Wednesday rejected a plan put forward by bondholders. That would have seen Tricap allowed to buy 10 million new shares for $5.50 each. That money would go to creditors along with 15 million shares which senior debenture holders could then buy for $5.50 each. Creditors would also share in $275 million of secured notes and an additional 1.1 million common shares.

If Tricap dropped out of Stelco's refinancing, the bondholders offered to arrange their own package. In another development yesterday, Stelwire workers in Hamilton voted 95 per cent in favour of a deal with the plant's new owner. Stelwire, with plants in Hamilton and Burlington, is one of the subsidiaries being sold by Stelco.

The pact will see the company's Burlington operation close and work consolidated in Hamilton. It includes an early retirement incentive that will allow workers age 55 with 15 years service to leave with a full pension.

"People are happy with this because we're going to restructure and put the business back on its feet," said union president Scott Duvall. "We're sad to be leaving the Stelco chain after 50 years, but we know we have to move on. Settling this will be a real burden off people's minds."

06 December 2005

Vincor - Holding Out

Vincor is doing diligence for the shareholders, hanging on for a deal. Last Jan, it hit a high of $36.78 CDN, and latest news is that they are close to a deal with Constellation. Is $40 too much? I thought Constellation would have paid a premium, since they want it bad enough. The current deal of a max of $35 expires 8 Dec. See what happens after that.

Nortel - Let's Move Up!

Nortel is cleaning house, to gain back double digit margins. Let's hope things get better in the new year.

05 December 2005

Personal Thoughts - US Steel

I have been watching steel for awhile, and most of the biggies had P/Es of less than 7 back in August. While USX looks good, I think its caught in the middle for size and value. Sure, they have cash on hand, however, China is expected to be a net exporter in 2006, with additional capacity coming online. I assume that this will hit USX a little harder to the bottom line, than what is being predicted, along with an expected drop in steel prices into Q2, to something below $500 US. I think USX may end up being someone's strategic partner sometime in 2006, before it goes on a spending spree for anyone in particular, and I don't think USX can get the same price as Dofasco. They must be due for some capital upgrades, so they will need the cash for that. Maybe a merge with AK? Anything is possible these days.

Personal Thoughts - Tim Horton's IPO

With Tim Hortons filing for IPO, my thoughts are going through the numbers to see what is the price I would pay...looking at the numbers, $600 million, for 15-18% of the total shares (based on what I had seen on Hoovers). Based on the aggressive revenue growth figures (7%), and based on last years earnings and revenue, I figure the cutoff for my interest is (base IPO price) around $50, which would be a steal at that price...nothing has been published yet, but Canadian investors may treat this like a Google equivalent for fast food, but I don't think it will go up as quickly in the short term...stay tuned. Rumours of an income trust for Canada's leading "to go" coffee are out there too.

28 November 2005

Dofasco and Vincor

Well, as I predicted, a white night came along...one of the 2 I was thinking that would. ThyssenKrupp is a German steelmaker, came in with a bid of $61.50... a little short on the $64 I thought Dofasco might get, but trading hit $63.90 on the TSX. Maybe Arcelor will sweeten the bid, but the sound of the board, it looks like a done deal.

Vincor is holding fast, expecting the shareholders to reject Constellation's current offer of $35. I still think they will come back in the new year. I will follow the run until Q4 2005 reports, and see if it will be a possible buy at $40 for Constellation.

Vincor is holding fast, expecting the shareholders to reject Constellation's current offer of $35. I still think they will come back in the new year. I will follow the run until Q4 2005 reports, and see if it will be a possible buy at $40 for Constellation.

27 November 2005

Thoughts and Comments for the end of November

Its been a quiet few days, due to US Thanksgiving. Here are a couple of things for Monday;

* Stelco vote tomorrow on the restructuring plan. Look for the stakeholders to accept it as is, and wipe out the common shares. More on when they come out of restructuring in January, as to whether they will be a good buy.

* Sony is having its problems. I still maintain that in Q1 2006, it will be depressed, and with news that Microsoft is selling Xboxs at a loss (software is the money maker), Sony should bounce back on the announcement of PS3 coming out. I heard that the PS3 can play any game on disk...if thats true, there may be more people lining up to buy those than the Xbox, due to older game inventories on the homefront.

* A while back, I mentioned that Walmart would be a big winner this season. Numbers out so far show that they did well this weekend, and will gain momentum over the holidays. I still think they will beat expectations next report. Overall shopping in the US was expected to be 22% better than last year.

That's all for now. Congrats to Edmonton on winning the Grey Cup!

* Stelco vote tomorrow on the restructuring plan. Look for the stakeholders to accept it as is, and wipe out the common shares. More on when they come out of restructuring in January, as to whether they will be a good buy.

* Sony is having its problems. I still maintain that in Q1 2006, it will be depressed, and with news that Microsoft is selling Xboxs at a loss (software is the money maker), Sony should bounce back on the announcement of PS3 coming out. I heard that the PS3 can play any game on disk...if thats true, there may be more people lining up to buy those than the Xbox, due to older game inventories on the homefront.

* A while back, I mentioned that Walmart would be a big winner this season. Numbers out so far show that they did well this weekend, and will gain momentum over the holidays. I still think they will beat expectations next report. Overall shopping in the US was expected to be 22% better than last year.

That's all for now. Congrats to Edmonton on winning the Grey Cup!

25 November 2005

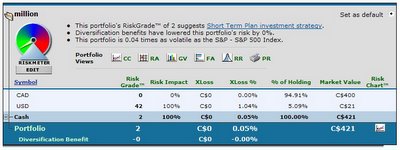

Updated Portfolio - November 2005

Just a quick update of the status of the cash account...

Still all cash, until the new year, and then I'll make the move over to an e-trade account.

Stelco Restructuring Plan

Looks like the restructuring plan for Stelco has been approved in principle with all stakeholders. Nothing for existing shareholders, so that was a bust. HOWEVER, even with everyone on board, Stelco is going to have a hard time making money when it comes out of bankruptcy in Jan 2006. We'll look at Stelco at the end of Q2 2006, to see if the new and improved Stelco is worth hedging for the last half of the year. Stay tuned. I figured that the governments would kick in $100 million to seal the plan - they ponied up $80 million...pretty good guess.

Note - the pension contribution holiday ends after 6 months after restructuring...so, look for charges of $30-$35 million against each of the Q3 & Q4 next year. We need to see the IPO of the new shares in Jan before we can crunch the numbers. Remember also, that GM just renewed the contract with Stelco, BEFORE it announced the plant closures.

Note - the pension contribution holiday ends after 6 months after restructuring...so, look for charges of $30-$35 million against each of the Q3 & Q4 next year. We need to see the IPO of the new shares in Jan before we can crunch the numbers. Remember also, that GM just renewed the contract with Stelco, BEFORE it announced the plant closures.

Dofasco Under Attack

News out on Wednesday, Arcelor put an offer out to the shareholders at $56...this was overdue. Dofasco has been a prime target for over a year, so it was just a matter of time. Of interesting note, was this excerpt from S&P the day of the announcement;

TORONTO (Standard & Poor's) Nov. 23, 2005--Standard & Poor's Ratings Services today said it placed its 'A-' long-term corporate credit and senior unsecured debt rating on Dofasco Inc. on CreditWatch with negative implications after Luxembourg-based Arcelor S.A. (BBB/Stable/A-2) announced a C$4.3 billion unsolicited cash offer for the company's shares. The CreditWatch stems from the likelihood that the ratings on Dofasco would be lowered two notches to be equalized with those on Arcelor if the transaction is completed.

My guess is that there will be someone else that comes into the picture and makes a grab for Dofasco. If I had to guess, Gerdau SA (or TK) might come in as white knights and compete. I think that it will be sold at $64, with QCM included.

TORONTO (Standard & Poor's) Nov. 23, 2005--Standard & Poor's Ratings Services today said it placed its 'A-' long-term corporate credit and senior unsecured debt rating on Dofasco Inc. on CreditWatch with negative implications after Luxembourg-based Arcelor S.A. (BBB/Stable/A-2) announced a C$4.3 billion unsolicited cash offer for the company's shares. The CreditWatch stems from the likelihood that the ratings on Dofasco would be lowered two notches to be equalized with those on Arcelor if the transaction is completed.

My guess is that there will be someone else that comes into the picture and makes a grab for Dofasco. If I had to guess, Gerdau SA (or TK) might come in as white knights and compete. I think that it will be sold at $64, with QCM included.

22 November 2005

Vincor - Can a Friendly Deal Be Done?

Vincor has taken its poison pill off the table, figuring that the shareholders will reject the current offer from Constellation Brands ($31). Current closing price is $34.80...look for Constellation to make another bid, paying a premium (20%?? - $6) over the current price. Of course, being the holiday season, this Q will show the numbers to support $40 or $41 offer price from Constellation (just a hunch...).

Stelco is still without a plan, with a current vote expected tomorrow. The only thing that will get everyone on-board will be another $100 million from the government...will they cave and give in? Maybe there is a creative way the government can come to the table, given the incentives coming down for the Big 3 auto.

RIM, closing down to $78.88, I still support the $62 target...

Disney is another up and comer to watch...stay tuned to see what happens with Pixar, and the lineup for the movies for 2006. They are off to a good start...look for earnings to beat the street.

Stelco is still without a plan, with a current vote expected tomorrow. The only thing that will get everyone on-board will be another $100 million from the government...will they cave and give in? Maybe there is a creative way the government can come to the table, given the incentives coming down for the Big 3 auto.

RIM, closing down to $78.88, I still support the $62 target...

Disney is another up and comer to watch...stay tuned to see what happens with Pixar, and the lineup for the movies for 2006. They are off to a good start...look for earnings to beat the street.

19 November 2005

Update - Miscellaneous

Just a few odds and ends this post;

* GM has sunk to a new low this week, which is making it attractive, if they can turn things around. Having a smaller market cap makes it an ideal takeover target, except for the $77 billion liabilities. Kerkorian might have some ideas in the weeks and months ahead.

* Stelco problems are continuing, with no vote yet. Monday (21 Nov) is the new date, and if the bondholders don't get on board, look for the provincial government to step in and increase their contribution.

* Here is my current "watch list" of stocks;

* GM has sunk to a new low this week, which is making it attractive, if they can turn things around. Having a smaller market cap makes it an ideal takeover target, except for the $77 billion liabilities. Kerkorian might have some ideas in the weeks and months ahead.

* Stelco problems are continuing, with no vote yet. Monday (21 Nov) is the new date, and if the bondholders don't get on board, look for the provincial government to step in and increase their contribution.

* Here is my current "watch list" of stocks;

Be sure to check back on a regular basis, as I keep tabs on what's happening in the markets.

15 November 2005

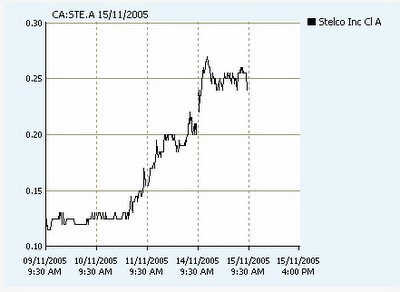

Stelco D-Day

Reviewing the action on Stelco, the chart below says it all;

Since the end of last week, Stelco has garnered almost 100% in value, of course, on the premise that the current restructuring plan will be voted down by bondholders. Stay tuned, lets see if we can get the 6 cents we were looking for a few weeks ago.

Since the end of last week, Stelco has garnered almost 100% in value, of course, on the premise that the current restructuring plan will be voted down by bondholders. Stay tuned, lets see if we can get the 6 cents we were looking for a few weeks ago.

13 November 2005

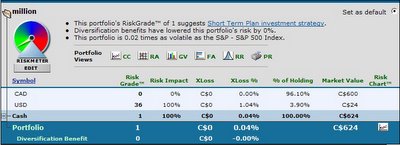

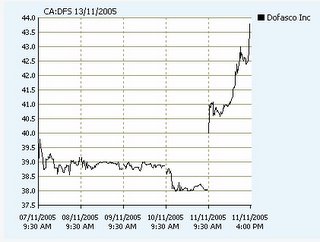

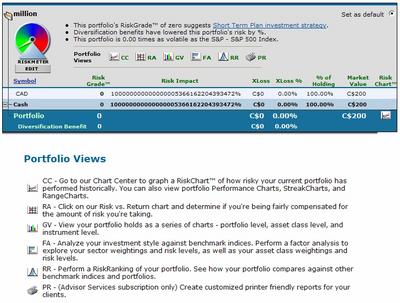

Updated portfolio

The following is a screen shot of my current portfoilio;

Look for better gains towards the end of the year, and reporting of Q4 results in Jan 2006, with DFS and the QCM units.

As we had discussed before, current holdings are cash, until there is enough (min. $500 to open an e-trade account)...looks like the target date for opening the account will be Jan 2006...stay tuned.

In other news, Dofasco climbed 13% on the day, on news of creation of an income trust for its QCM holdings.

Look for better gains towards the end of the year, and reporting of Q4 results in Jan 2006, with DFS and the QCM units.

11 November 2005

Explanation of Income Trusts

Income trusts are the latest craze, and Dofasco has spun off QCM into one. Check out Wikipedia explanation on income trusts.

Vincor Being Stalked

Latest news is Constellation Brands is looking to pick up Vincor, with the value being pegged at about +20% from the current value ($34.81)...might be worth looking into getting a few shares to cash in on the acquisition. More, if they pay a premium.

10 November 2005

Odds and Ends

A couple of things tonight to note...Stelco shares jumped 16%, from 13 cents to 16 cents, probably on the pending news of the restructuring plan being voted down...on that note, Stelco lost $42 million this quarter. Keep in mind that even when they come out of restructuring, the price of steel won't be able to sustain Stelco's proposed restructure. Look for losses for quarters to come, until there are some concessions from the union.

Nortel is down a bit...it will bounce back...

Nortel is down a bit...it will bounce back...

09 November 2005

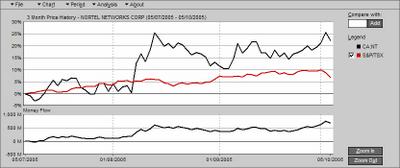

Nortel Status

Nortel is still up and down this week...hopefully it gains momentum over the next 6 weeks...click here for the latest chart.

The Next Big Techs?

Here is an excerpt from FSB with respect to a business plan competition and how startups rated.

I like the idea of a gaming card that compensates for lag. This would be a cheaper alternative to people out there with older PCs that don't want to spend the money on a faster computer...just a thought...

On the Stelco front, bondholders are holding their ground about vetoing the restructuring plan, and the shares moved up 13% today (11 cents to 13 cents on the TSX), with debentures dropping down 6%...CEO Pratt will have to work wonders to get everyone on board. Big vote is scheduled for 15 Nov....stay tuned.

I like the idea of a gaming card that compensates for lag. This would be a cheaper alternative to people out there with older PCs that don't want to spend the money on a faster computer...just a thought...

On the Stelco front, bondholders are holding their ground about vetoing the restructuring plan, and the shares moved up 13% today (11 cents to 13 cents on the TSX), with debentures dropping down 6%...CEO Pratt will have to work wonders to get everyone on board. Big vote is scheduled for 15 Nov....stay tuned.

05 November 2005

The Next Tidal Wave in Advances

I was reading Business Week Online, and came across an interesting article...and excerpt is below;

Today, the signs around us are just as difficult to read, but, as Yogi Berra once remarked, "You can see a lot just by looking." What will be the next half-century's all-transforming technology? And who will reap the riches to become the next Bill Gates?

SIGNS OF CHANGE. I believe the answer lays in the confluence of three heretofore largely separate trends:

• The evolution of semiconductor-manufacturing capabilities and products into nanoscale dimensions.

• The increasing ability of biochemists to engineer genetic material at the molecular (nano) level.

• The exponential growth of computer simulations permitting the design of clusters of atoms at the nano dimension.

For decades, each trend evolved separately. But today, these trends have come together, amplifying each other's capabilities and forming the nucleus of what I call the 3N revolution.

SIZZLING SYNERGIES. Why these three trends?

First, they are each attracting huge numbers of very smart scientists and engineers from around the world -- and one should never underestimate the potential of combined intellectual horsepower.

Second, all three trends are already beginning to overlap in highly productive ways. The gene chips from a company like Affymetrix rely on semiconductor processing in their manufacture, new materials are now made directly in the computer rather than empirically on the lab bench, and the Human Genome Project depended as much on high-speed numerical analysis as on wet chemistry.

Today, the signs around us are just as difficult to read, but, as Yogi Berra once remarked, "You can see a lot just by looking." What will be the next half-century's all-transforming technology? And who will reap the riches to become the next Bill Gates?

SIGNS OF CHANGE. I believe the answer lays in the confluence of three heretofore largely separate trends:

• The evolution of semiconductor-manufacturing capabilities and products into nanoscale dimensions.

• The increasing ability of biochemists to engineer genetic material at the molecular (nano) level.

• The exponential growth of computer simulations permitting the design of clusters of atoms at the nano dimension.

For decades, each trend evolved separately. But today, these trends have come together, amplifying each other's capabilities and forming the nucleus of what I call the 3N revolution.

SIZZLING SYNERGIES. Why these three trends?

First, they are each attracting huge numbers of very smart scientists and engineers from around the world -- and one should never underestimate the potential of combined intellectual horsepower.

Second, all three trends are already beginning to overlap in highly productive ways. The gene chips from a company like Affymetrix rely on semiconductor processing in their manufacture, new materials are now made directly in the computer rather than empirically on the lab bench, and the Human Genome Project depended as much on high-speed numerical analysis as on wet chemistry.

03 November 2005

More on Stelco's Situation

Interesting article on Stelco situation...

Court deliberates over Stelco

by Laura King in Toronto3 November 2005

TheDeal.com Copyright 2005, The Deal, LLC. All Rights Reserved

The Ontario Court of Appeal has reserved its decision on whether to throw out two financing deals that form the crux of the restructuring plan for insolvent steelmaker Stelco Inc.

The three-judge panel said Wednesday, Nov. 2, it will rule promptly, but Stelco CEO Courtney Pratt said the company must make changes to the restructuring plan to satisfy the bondholders who oppose the deal.

Meanwhile, Stelco announced that it is selling three of its units to Mittal Steel Co. NV. Stelco creditors are to vote on the its restructuring plan on Nov. 15 but a group of bondholders, including some U.S. hedge funds, say they'll veto it.

The group opposes two deals included in the plan. The restructuring plan requires approval by creditors holding at least two-thirds of the money owed, or about C$640 million ($545 million).

"We shouldn't kid ourselves,'' Pratt said outside court. "This plan is not going to get accepted.'' Stelco has been under creditor protection since January 2004. Justice James Farley of the Ontario Superior Court approved its restructuring plan on Oct. 4. It includes a deal with the Ontario government for a C$100 million loan that is contingent on Stelco making a C$400 million down payment on its C$1.3 billion pension solvency deficit, which the bondholders say is excessive. Under that deal, $75 million of the C$100 million loan can be forgiven and the province could end up owning 8% of the Stelco.

A second deal calls for Brascan Corp.'s Tricap Management Fund to provide C$450 million in financing but the bondholders say fees associated with the deal are too high. The bondholders say Stelco didn't actively seek competing proposals.

Tricap could end up with a multimillion dollar breakup fee if the deal collapses. Lawyers for bondholders argued Wednesday that Farley shouldn't have approved the restructuring plan knowing that the bondholders intend to vote against it.

Bondholders would be paid about 66 cents on the dollar under Stelco's restructuring plan, which would be more than creditors of Bethlehem Steel Corp. and other U.S. steelmakers received after restructuring. Stelco shareholders would end up with nothing.

Stelco is aiming to exit creditor protection by Dec. 31. Stelco said it has signed a letter of intent with Mittal and that the sale hinges on the negotiation of a definitive agreement. It didn't disclose a price for the sale of Norambar Inc. in Contrecoeur, Quebec, Stelfil Ltée. in Lachine, Quebec, and Stelwire Ltd. in Ontario.

Stelco announced early in its restructuring process that it would sell the divisions, which it considers noncore, in order to focus on its integrated steel business.

Court deliberates over Stelco

by Laura King in Toronto3 November 2005

TheDeal.com Copyright 2005, The Deal, LLC. All Rights Reserved

The Ontario Court of Appeal has reserved its decision on whether to throw out two financing deals that form the crux of the restructuring plan for insolvent steelmaker Stelco Inc.

The three-judge panel said Wednesday, Nov. 2, it will rule promptly, but Stelco CEO Courtney Pratt said the company must make changes to the restructuring plan to satisfy the bondholders who oppose the deal.

Meanwhile, Stelco announced that it is selling three of its units to Mittal Steel Co. NV. Stelco creditors are to vote on the its restructuring plan on Nov. 15 but a group of bondholders, including some U.S. hedge funds, say they'll veto it.

The group opposes two deals included in the plan. The restructuring plan requires approval by creditors holding at least two-thirds of the money owed, or about C$640 million ($545 million).

"We shouldn't kid ourselves,'' Pratt said outside court. "This plan is not going to get accepted.'' Stelco has been under creditor protection since January 2004. Justice James Farley of the Ontario Superior Court approved its restructuring plan on Oct. 4. It includes a deal with the Ontario government for a C$100 million loan that is contingent on Stelco making a C$400 million down payment on its C$1.3 billion pension solvency deficit, which the bondholders say is excessive. Under that deal, $75 million of the C$100 million loan can be forgiven and the province could end up owning 8% of the Stelco.

A second deal calls for Brascan Corp.'s Tricap Management Fund to provide C$450 million in financing but the bondholders say fees associated with the deal are too high. The bondholders say Stelco didn't actively seek competing proposals.

Tricap could end up with a multimillion dollar breakup fee if the deal collapses. Lawyers for bondholders argued Wednesday that Farley shouldn't have approved the restructuring plan knowing that the bondholders intend to vote against it.

Bondholders would be paid about 66 cents on the dollar under Stelco's restructuring plan, which would be more than creditors of Bethlehem Steel Corp. and other U.S. steelmakers received after restructuring. Stelco shareholders would end up with nothing.

Stelco is aiming to exit creditor protection by Dec. 31. Stelco said it has signed a letter of intent with Mittal and that the sale hinges on the negotiation of a definitive agreement. It didn't disclose a price for the sale of Norambar Inc. in Contrecoeur, Quebec, Stelfil Ltée. in Lachine, Quebec, and Stelwire Ltd. in Ontario.

Stelco announced early in its restructuring process that it would sell the divisions, which it considers noncore, in order to focus on its integrated steel business.

01 November 2005

Top Stocks to Watch - CNN Money's Sivy's 70

CNN Money has a few good newsletters that come out, that provides some understanding as to what is happening in the market that day. Also, Sivy is one of the correspondents, and he has done an excellent job of listing the top 70 stocks of major players, which he thinks will provide above market average growth in the long term.

Nortel clears last hurdle, we hope

Nortel and Motorola have settled their lawsuit for the new CEO. Q3 results will be posted on Wed. Last closing price was $3.81.

27 October 2005

Research in Motion - Legal Problems

Interesting to note, that, RIM has lost about 30% of its value, due to legal issues. The Supreme Court denied a request to suspend a lower court's ruling in a key patent infringement lawsuit with NTP.

On an interesting note, there were terms of an agreement that was drafted earlier this year, but lacked a meeting of the minds to seal the deal, which includes for licensing arrangements.

So, whats the future hold in store?

I think RIM will bounce back relatively quickly, although not to the same high levels as before. Some analysts are picking target prices of around $62...it will just be a matter of how much NTP will agree to settle for. My guess is a modest premium above the last one, with RIM taking the hit in Q1 2006, so look for improvements after that. RIM will sign quickly, as the technology is partnered with others.

On an interesting note, there were terms of an agreement that was drafted earlier this year, but lacked a meeting of the minds to seal the deal, which includes for licensing arrangements.

So, whats the future hold in store?

I think RIM will bounce back relatively quickly, although not to the same high levels as before. Some analysts are picking target prices of around $62...it will just be a matter of how much NTP will agree to settle for. My guess is a modest premium above the last one, with RIM taking the hit in Q1 2006, so look for improvements after that. RIM will sign quickly, as the technology is partnered with others.

26 October 2005

I'm Back...

Sorry for the lack of updates everyone, but I have been busy at work, and I have had no time to really look into investing and stocks until now...after this weekend, I will be able to contribute to the blog more regularly.

Anyways, since the last entry, it has been time to deposit to the cash account, to build up enough for opening an e-trade account. Balance stands at $321, which includes a deposit of $100 CAD, and I found some USD laying around, and added that to it...hence the $321. Every dollar helps!

Anyways, since the last entry, it has been time to deposit to the cash account, to build up enough for opening an e-trade account. Balance stands at $321, which includes a deposit of $100 CAD, and I found some USD laying around, and added that to it...hence the $321. Every dollar helps!

In other news, Nortel is being played by the profit takers, so it has been up and down around $4 for the past 2 weeks.

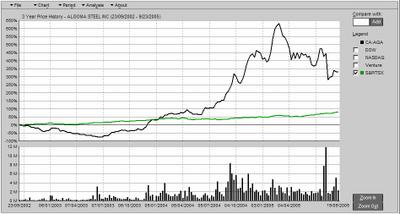

I had suggested Stelco, to see if we could get in and speculate the loss of votes for the restructuring plan currently on the table...it hasn't panned out that way yet, and rumour has it that the current plan will yield 66% to creditors (through equity and shares), versus 17-33% if the plan is voted down, and the company left to sell off assets. It is currently at 15 cents. In related news, Mittal paid a premium for the Ukraine state-owned mill, of $4.8 billion, expecting the steel market to rebound from where it is now...as a result, look for low P/E steel stocks to make some ground in Q1 2006. Algoma is holding on to a lot of cash, but hasn't decided what to do with it. Paulson, whose company holds 19%, is asking for a cash dividend, putting pressure on the board to do that. With a low P/E, prices going up in Q1 2006, look for a substantial return on Algoma in the next 6-9 months.

17 October 2005

Nortel is even a better pick now...

If you have been reading this blog for the last 2 months, you know I am a Nortel fan...

Nortel is making some changes at the top...see the article here.

As a result, Nortel closed at 4.10 today...look for big things to happen in the next few quarters.

Nortel is making some changes at the top...see the article here.

As a result, Nortel closed at 4.10 today...look for big things to happen in the next few quarters.

11 October 2005

Spam Stock Tips....Are They Worth It?

Ever wonder if you missed out on an opportunity with all those emails that give you "tips"? This site tracks a few of them, and shows the track record...

http://www.spamstocktracker.com/

Don't ever think you have missed out on a good trade when you read these emails!

http://www.spamstocktracker.com/

Don't ever think you have missed out on a good trade when you read these emails!

Finding Value in Markets...

I was doing some searching on CNN Money, and came across this link, which gives some good indications of the value of a stock. One of the best comparators to the value of the stock, is to the S&P 500 P/E ratio. Now, there are other considerations to determine whether its a great value, but 2 benchmarks are that the S&P 500 have returned about 12%/year, with an average P/E of approx. 16.5...anything lower, with the potential to garner growth greater than the P/E (that is, growth%/PE ratio >1), then look for it to perform better than the index.

Keep in mind, you still need to look at the company in more detail, but the above should weed out a few stocks you may be interested in.

I am looking at a few stocks now, and will blog about them later in the week when I do a little more digging.

Keep in mind, you still need to look at the company in more detail, but the above should weed out a few stocks you may be interested in.

I am looking at a few stocks now, and will blog about them later in the week when I do a little more digging.

10 October 2005

Bankruptcy Details on Stelco...Questions Answered

I came across this article, courtesy of the Hamilton Spectator...it gives some answers into some bankruptcy questions, specifically related to Stelco, but they are the worst case...some interesting information when looking at "stressed" companies and their stock...

The great Stelco guessing game

How did we get here? What's at stake? What happens next?

8 October 2005 Copyright (c) 2005 The Hamilton Spectator.

Stelco has teetered on the brink of collapse so many times in the last 20 months, it's almost become routine. In less than two years since the steelmaker sought bankruptcy protection, there have been marathon negotiations, countless court dates, bankruptcy protection extensions and enough lawyers to populate a small country.

Add to that a scant bankruptcy act that leaves those lawyers lots of wiggle room and you have a situation that would confuse even the most brilliant legal or economic mind.

So what's the situation all about and what does it mean? Here's a look at the essential elements of the latest in the steelmaker's fight to get out of bankruptcy.

What is the Companies' Creditors Arrangement Act?

The CCAA is the bankruptcy protection legislation which allows Stelco to put off paying its creditors until it has reorganized.

Unlike its predecessor -- the Bankruptcy and Insolvency Act -- this depression-era legislation is short on strict deadlines and structure.

Why did Stelco seek that protection in the first place?

Stelco CEO Courtney Pratt said the company had no choice. The board of directors said the steelmaker was poised to run out of cash within months. It had lost $168 million in the first nine months of 2003, had a $545-million, long-term debt and was $1.3 billion short of what it needed to cover pension obligations.

Since then, booming steel prices have made unprecedented profits, prompting unions to argue the company wasn't really insolvent in the first place.

Why has the company needed so many bankruptcy protection extensions?

It's not uncommon for companies to get bankruptcy protection extensions but Stelco's 11 extensions have set something of a record.

Steel expert Peter Warrian said this restructuring has been painfully drawn out because of the large number of stakeholders who need to agree. Plus, the University of Toronto professor said, rising steel prices and soaring profits made the situation seem much less dire, sapping any willingness to compromise.

Stelco is poised to request its 12th and, hopefully last, extension Dec. 2. What has the company been doing these last 20 months? Besides requesting bankruptcy protection extensions, the company and its unions have been hard at work -- taking turns bickering, negotiating and shopping around for the best financing deal.

The steelmaker's unions spent the first few months of bankruptcy protection fighting Stelco's insolvency claim in court. When that was rejected, they started negotiating a new collective agreement for Lake Erie workers.

At the same time, both sides searched for a financing deal. After a number of bids, Stelco and its unions settled on the Tricap deal.

What is the Tricap deal?

Under the deal, the province chips in $100 million towards the pension shortfall while Tricap gives Stelco a $350-million renewable loan secured to the steelmaker's assets. Tricap also insures Stelco's attempt to get another $75 million through the sale of secured notes -- IOUs which can be converted into stock.

The deal gives unsecured creditors $225 million in secured notes and $300 million in the form of unsecured notes which can be converted into shares.

In return, Stelco will give Tricap $1.6 million for expenses and pay a $10.75 million "commitment fee" which Tricap keeps if the deal falls through.

Who supports the deal?

Stelco is on board, as are the company's salaried retirees and the unions representing AltaSteel and Lake Erie workers.

Who wants to see the deal killed?

Stelco's largest union, Local 1005 which has boycotted the restructuring negotiations, says the deal poses "enormous risks" and doesn't address the core problems facing the company.

But the bondholders are the deal's most powerful opponents. Bondholders, the steelmaker's largest group of unsecured creditors, are hoping to get a better deal which pays them in hard cash rather than in Stelco stocks.

Who are the bondholders and why do they have so much power?

Bondholders are a mysterious and anonymous group of investors. Sometimes called "vulture capitalists," they often buy up cheap bonds from nervous investors when a company is in trouble.

They then use their influence during the restructuring process to increase the value of their bonds and make a profit. Their influence, in this case, is considerable. Because they make up the majority of the steelmaker's unsecured creditors, they have a deciding vote on any financing deal and could effectively kill it.

The unsecured creditors are scheduled to vote on the Tricap deal Nov. 15.

How does their vote Nov. 15 work?

Every dollar owed equals one vote on Nov. 15. Since $660 million is owed, there will be 660 million votes cast. The bondholders -- with the most money invested in Stelco -- will cast the majority of those votes.

Each of the five companies under the Stelco umbrella will be voted on separately. The votes will be counted by the end of the day. A location for the vote has yet to be determined.

What happens if they vote it down?

It won't be the first time. Bondholders voted down an endorsed deal in the restructuring of Algoma Steel. They were ordered into a hotel with the company, not to emerge until they had a deal. Several days later, they had one.

But if the bondholders vote down the Tricap deal, it will die. Pratt said it would then be up to Farley whether to liquidate the company or have it emerge from bankruptcy without a plan -- neither of which, he said, are good for the company.

What happens if they vote in favour?

Even then, Stelco wouldn't be out of the woods. The deal then goes back to Farley's courtroom. That's when Farley will hear objections to the deal, possibly from shareholders, and decide whether to approve it or not.

In the end, whether Stelco emerges intact or is liquidated rests in his hands.

Could bondholders kill the deal before November?

They are doing their utmost to do exactly that. Bondholders launched a court appeal Thursday, objecting to Farley's tentative approval of the Tricap deal. If the appeal is successful, it will essentially kill the Tricap deal.

What happens to shares and shareholders under this deal?

Stelco shares won't be worth the paper they're written on if this deal is done. Since they are at the bottom of the bankruptcy food chain, they are going to be left with nothing to show for their investment. They could launch a long and expensive lawsuit to recover some of their money but experts say it's a fight they will likely lose.

What role do the unions play?

Unions have a lot of leverage in this restructuring. That's because workers at Lake Erie and AltaSteel both had strike mandates and the renegotiation of their collective agreements became tied to the restructuring process.

Local 1005 is not in the same boat -- because they have a valid collective agreement, they are not in a legal strike position.

While the Lake Erie and AltaSteel locals have a new collective agreement, their members won't vote on their new collective agreement until after bondholders have voted on the Tricap deal.

That essentially gives union members a final say on the restructuring plan, so Stelco will have to keep their interests in mind as it negotiates with the bondholders.

What happens the day after Stelco emerges from bankruptcy?

If all goes well, come Jan. 1 it will be business as usual at the steel mills. But Pratt said Stelco will emerge from bankruptcy a completely different company, free from creditors since it will have paid them all off by the time the bankruptcy protection is lifted. It will have a new board of directors and a new financial plan while its management will remain intact.

How long does it take for a company to get back on its feet?

There can be profit after bankruptcy. Algoma Steel just had its most profitable year in more than a century in business. But it had to go through two major restructurings -- one in 1991 and another in 2001 -- and lay off 600 workers before it hit its stride this year.

It's anyone's guess how long it will take for Stelco to post a profit once it emerges from bankruptcy, but the steelmaker has been making fistfuls of money throughout its bankruptcy protection thanks to a spike in steel prices.

What happens to Hamilton if Stelco doesn't survive?

Hamilton doesn't have its reputation as Steeltown riding just on the survival of Stelco. There are at least 16,000 jobs in Hamilton related to the steelmaking and processing industry. Then there are at least 500 Hamilton companies who deal with the steel industry.

City hall is equally concerned about Stelco's fate. The city's coffers get $10.5 million in taxes from the steelmaker, plus $4.5 million toward education.

The great Stelco guessing game

How did we get here? What's at stake? What happens next?

8 October 2005 Copyright (c) 2005 The Hamilton Spectator.